Demand for hay is firming in Australia [News Oceania n ° 6/2018]

19/03/2018

The growing taste for Italian dairy

26/03/2018South America needs butterfat [News South America n°6/2018]

Period: March 5 – 16, 2018 Dryness and high summer temperatures persist in the main dairy basins of Argentina and Uruguay, increasing heat stress on dairy herds and decreasing the quality of the […]

Period: March 5 – 16, 2018

Dryness and high summer temperatures persist in the main dairy basins of Argentina and Uruguay, increasing heat stress on dairy herds and decreasing the quality of the pastures.

Nevertheless, milk volumes are sufficient for most processing needs. Fluid and UHT milk demands remain robust. The upcoming fall holiday season supports the interest for cream, but cream availability is very tight.

As reported by the government, in February 2018 Argentina milk production has been +14% higher than Feb 2017, while nominal farmgate milk price increased by +15%.

In Brazil milk production decreases seasonally, and the lower milk (and cream) supply supports farmgate milk prices. The demand for butterfat is strong, and the current cream intakes are less than sufficient to cover all manufacturing needs. Cheese sales are light to moderate while inventories are ample.

Processors are focusing drying schedules on WMP: SMP supply is limited, but still more than sufficient. Consequently, SMP export prices decreased, anticipating the decrease at GDT event on March 20.

Demand for WMP is good, but WMP inventories are less than adequate to meet buyers and end users’ needs: WMP export prices increased consequently.

See all the information in the new webpage dedicated to the dairy market in South America on CLAL.it >

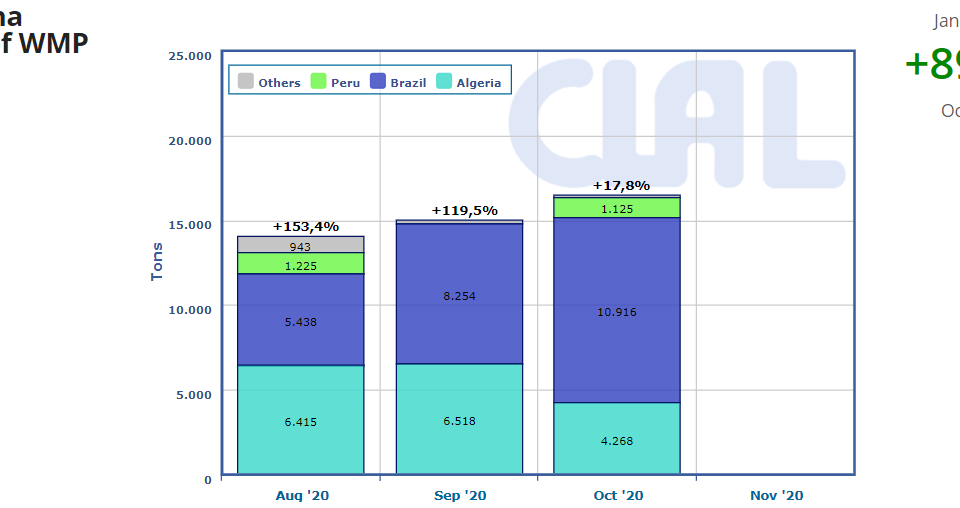

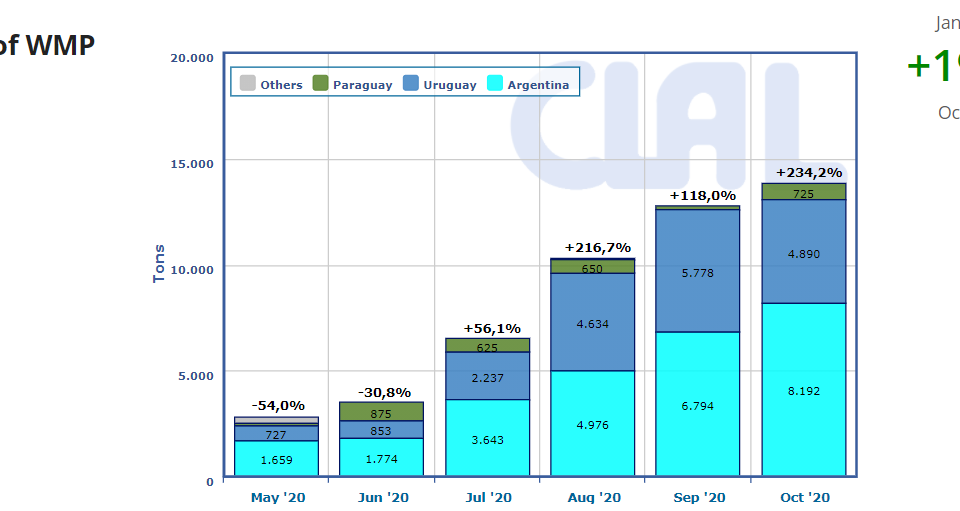

CLAL.it – WMP export prices in South America

{kind=link}

{kind=link}